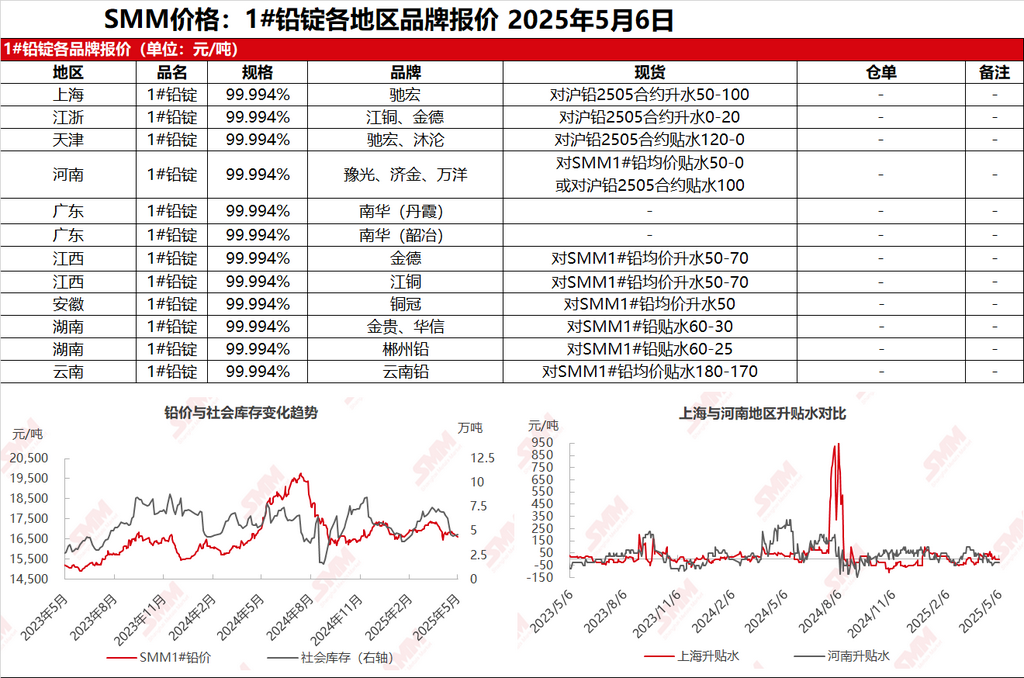

SMM reported on May 6: In the Shanghai market, Chihong lead was quoted at 16,685-16,770 yuan/mt, with premiums of 50-100 yuan/mt against the SHFE lead 2505 contract. In Jiangsu and Zhejiang, JCC and Jinde lead were quoted at 16,635-16,690 yuan/mt, with premiums of 0-20 yuan/mt against the SHFE lead 2505 contract. Following the Labour Day holiday, SHFE lead prices opened lower. Some suppliers raised their premiums and discounts, while others actively sold off, keeping their premiums and discounts unchanged from before the holiday. The discounts for cargoes self-picked up from primary lead smelters narrowed, with mainstream production areas quoting discounts of 100-40 yuan/mt against the SHFE lead 2506 contract ex-factory. Secondary lead smelters were generally reluctant to sell at low prices, resulting in fewer quotations. Traders, however, offered lower prices, with secondary refined lead quotations at discounts of 100-0 yuan/mt against the SMM 1# lead average price ex-factory. Additionally, downstream enterprises, in the early stages of production resumptions, maintained a cautious attitude towards the decline in lead prices. Inquiries increased, but actual transactions remained low.

Other markets: Today, the SMM 1# lead price fell by 100 yuan/mt from the previous trading day. In Henan, traders offered discounts of 100 yuan/mt against the SHFE lead 2506 contract. In Jiangxi, smelters quoted premiums of 50-70 yuan/mt against the SMM 1# lead average price ex-factory. In Hunan, smelters offered discounts of 50-30 yuan/mt against the SMM 1# lead average price ex-factory, while traders quoted discounts of 60-50 yuan/mt against the SMM 1# lead average price. On the first trading day after the holiday, lead prices weakened. Downstream enterprises were hesitant to purchase due to fears of further price declines, resulting in generally weak market transactions.